Jon Tetzlaff/iStock Editorial via Getty Images

Synopsis

XPO, Inc. (NYSE:XPO) specialises in providing freight transportation services. For its most recent 2Q24 results, consolidated revenue grew 8.5% year-over-year, reaching $2.079 billion. This growth was driven by both of its reportable segments, North American Less-Than-Truckload and European Transportation. Additionally, its adjusted margins expanded year-over-year.

Due to XPO’s commitment and focus on improving service quality, it has led to record-high yields and significantly reduced damage claims. Its yield reached an all-time high of $23.56, while damage claims as a percentage of revenue continued to decrease to a record low of 0.2%. Additionally, XPO’s investment in its network capacity shows no signs of slowing down. Although the current freight industry is soft, XPO stated that it is stable. Given XPO’s performance and commitment to improving the business, which is bearing results, I am reiterating my buy rating.

Recap Of Previous Coverage

In my previous post on XPO, I recommended a buy rating for the company when it was trading at around $107. Currently, the share price has increased beyond that. The buy recommendation stems from several factors, which I will provide a recap of. XPO was committed to investing in expanding its network capacity. Combined with its strong market positioning and vast market reach, this was expected to bolster and support its growth. In addition, XPO focused on improving and providing high-quality services. This commitment resulted in lower damage claims and higher yield.

Investment Thesis

Due to XPO’s continuous effort on improving service quality, it has achieved record-high yields as well as record-low damage claims. When combining the low damage claims with XPO’s on-time performance and fast network, it is creating a competitive advantage for itself and differentiating it from others. As a result, this is leading to an improvement in volume. Combining higher yield with improved volume is driving XPO’s growth. Even in the current soft freight market, XPO’s effective strategic initiatives have positioned itself to outperform. Apart from service quality, it is also continuing to invest in network capacity to reduce cost and further scale the business. This initiative allows XPO to strike when opportunities arise.

Service Excellence Drives Record-Low Damage Claims And Yield Growth

Investor Relations

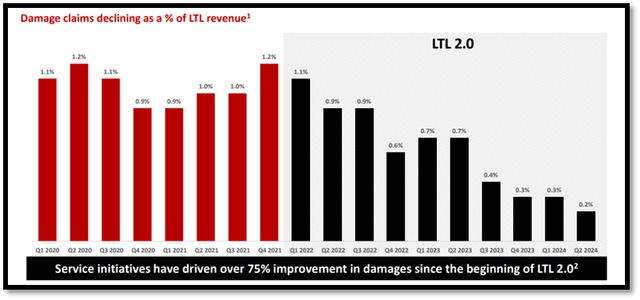

Starting with damage claims, the chart above shows that damage claims as a percentage of LTL revenue have decreased to 0.2%, a record level for XPO. Before the implementation of LTL 2.0, the damage claim rate was around 1%, with a peak of 1.2%. This implies that the frequency of damage claims has been reduced by approximately 80%.

When combined with XPO’s improved on-time performance and its fastest networks for one- and two-day lanes, this creates a competitive advantage for XPO, differentiating it from its competitors. As a result, it leads to improved yield and volume.

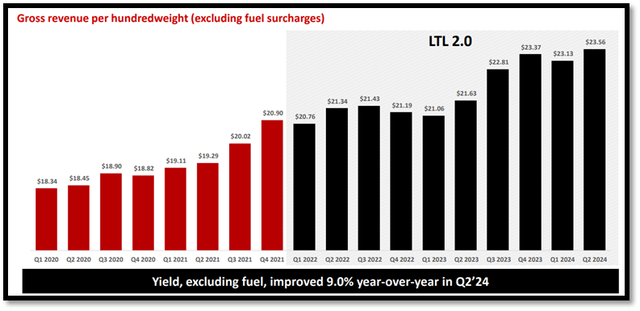

Looking at the following chart, gross revenue per hundredweight, or yield, has been consistently increasing since 1Q20. Back then, yield was $18.34, and as of 2Q24, it has increased to $23.56. In fact, this is one of the highest levels recorded ever since the start of LTL 2.0.

Investor Relations

Investment In Network Expansion Enhances Capacity And Efficiency

Investor Relations

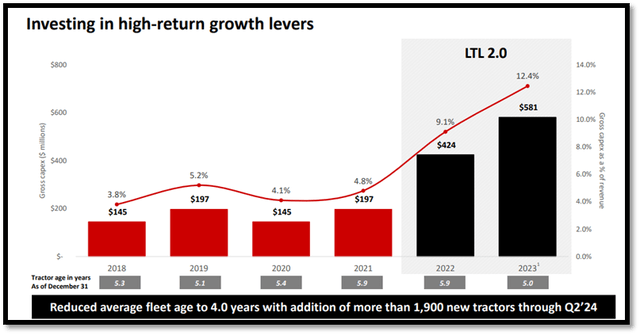

Even as of today, XPO’s commitment to investing in network capacity in order to improve service quality is not showing signs of slowdown. As of 2023, XPO’s gross capex invested has increased to $581 million, almost triple the amount it invested back in 2018. Additionally, the average age of tractors was around 5 years as of 2023.

Year to date, XPO added an additional 1,900 new tractors, thus driving down the average age to 4 years. As the new tractors are much more efficient to operate, and with average age reduced, it resulted in a double-digit decline in 2Q24’s maintenance cost for XPO.

In addition, year-to-date, XPO also manufactured more than 2,600 trailers. XPO is the only US freight transportation firm that produces its own trailers. This ability will allow XPO to increase capacity as needed when the cycle recovers.

Moving on to the 28 service centres XPO acquired last year, so far, it has opened 14 of them. Another 10 are expected to begin operation in the second half of 2024. The remaining 4 will start by early 2025. As these service centres are located in freight markets with high-growth potential, these additional centres are expected to bolster XPO’s outlook when the market recovers, as it will expand XPO’s capacity. Additionally, the larger footprint also places XPO closer to customers and minimises the need for freight re-handling.

Strong 2Q24 Earnings Results And Segment Performance

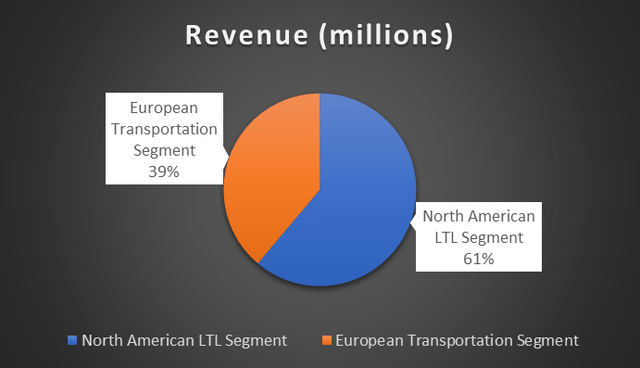

A quick recap on XPO: it specialises in providing freight transportation services. The company has two reportable segments: North American Less-Than-Truckload [LTL] and European Transportation. The North American LTL segment is the largest component of its overall business. Based on 2Q24 revenue, this segment accounts for 61% of XPO’s total revenue, while the European Transportation segment accounts for the remaining 39%.

Author’s Chart

XPO released its 2Q24 earning results on August 1, 2024. Its total revenue grew 8.5% year-over-year from $1.917 billion to $2.079 billion. This high single-digit percentage growth was driven by both of its reportable segments, which are North American Less-Than-Truckload and European Transportation. For the quarter, both segments’ revenue increased 12% and 3.5% year-over-year, respectively.

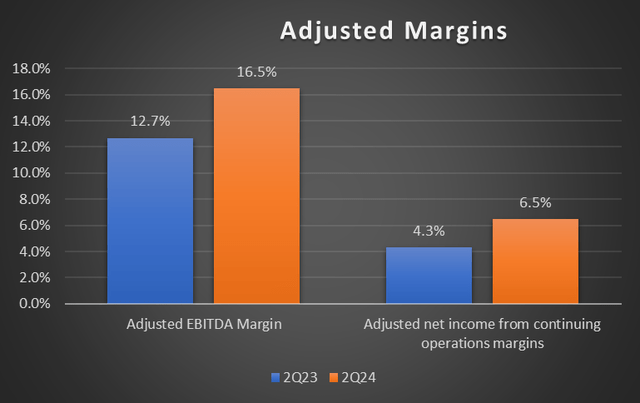

Moving on to margins, operating income increased 84.1% year-over-year from $107 million to $197 million. In terms of adjusted EBITDA, it increased 40.6% year-over-year from $244 million to $343 million. 2Q24’s adjusted EBITDA margin was 16.5% vs. previous period 12.7%. The expansion in adjusted EBITDA margin was driven by margin expansion in both the reportable segment and effective corporate expense management. For the quarter, corporate net expense decreased by 70% to $3 million. On the other hand, XPO’s 2Q24 adjusted net income from continuing operations margin expanded from 4.3% to 6.5%.

Looking at the following table, the North American Less-Than-Truckload segment’s adjusted operating income was up 50.7% while adjusted EBITDA increased 42.8%. For its European Transportation segment, adjusted operating income increased 5.6% while adjusted EBITDA increased 6.5%. These growths were attributed to XPO’s pricing gains, cost management initiatives, and volume increase. As a result, XPO’s adjusted diluted EPS increased from $0.71 to $1.12, which represents year-over-year growth of 57.7%.

10Q Author’s Chart

North American LTL Segment

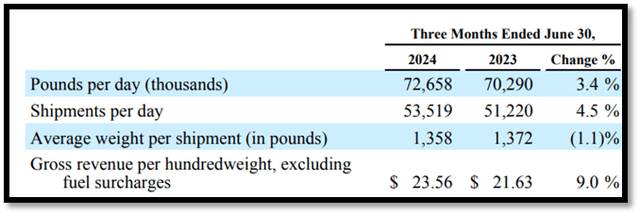

For 2Q24, XPO’s North American LTL segment revenue was up approximately 12% year-over-year to $1.272 billion. For the previous period, revenue reported was $1.136 billion. Excluding fuel surcharge revenue, revenue year-over-year growth was higher at 13.2%. This growth was driven by both higher gross revenue per hundredweight and volume. The increase in gross revenue per hundredweight and volume was due to XPO’s commitment to improve service quality. For context, 2Q24 fuel surcharge revenue was $208 million while the previous period was $196 million. The following table shows the metrics used to evaluate the performance of XPO’s North American LTL segment.

10Q

2Q24’s yield, which is measured by gross revenue per hundredweight excluding fuel surcharges, increased 9% year-over-year to $23.56 from the previous period’s $21.63. This high single-digit percentage increase was attributed to pricing initiatives. On the other hand, the volume increase, which is measured in pounds per day, was driven by higher shipments per day, partially offset by a modest decline in average weight per shipment.

European Transportation Segment

Moving on to XPO’s European Transportation segment, revenue was up 3.5% year-over-year from $781 million to $808 million, despite the soft macroeconomic environment. This growth was attributed primarily to higher yield and volume. Additionally, XPO was able to carry out strong pricing actions that outpaced inflation.

Additionally, the segment’s 2Q24’s EBITDA increased by 7% year over year, marking the highest level since 2019. This strong EBITDA growth was attributed to growth in revenue as well as disciplined and effective cost control measures. For context, the UK and France reported the strongest EBITDA growth. The UK’s EBITDA growth was in the high teens, while France was in the high single-digit percentage. UK is considered an important market for XPO.

On an adjusted basis, adjusted EBITDA margin for 2Q24 was 6.1%, a modest improvement compared to the previous period of 6%. The improvement in adjusted EBITDA margin was attributed to a decrease in fuel cost but partially offset by an increase in salaries, wages, and employee benefits.

Apart from strong revenue and EBITDA growth, sales pipeline has increased to $1.3 billion, a record. Additionally, XPO’s European Transportation segment continues to gain new business from blue-chip customers, further strengthening and solidifying its position in key European geographies.

Relative Valuation Model

Author’s Relative Valuation Model

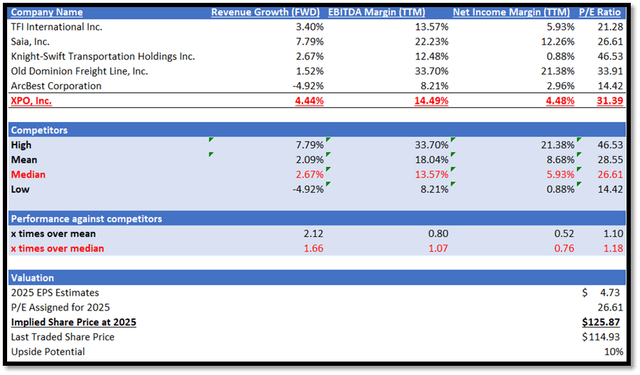

A quick recap: XPO operates in the cargo ground transportation industry, according to Seeking Alpha. In my relative valuation model, I will be comparing XPO against its peers in terms of growth outlook and profitability margins.

Starting with growth outlook, XPO outperformed its peers’ median. XPO has a forward revenue growth rate of 4.44%, which is higher than peers’ median of 2.67%, or 1.66x over the median. In terms of profitability margins trailing twelve months [TTM], XPO performance is mixed. XPO reported EBITDA margin TTM of 14.49%, which outperformed peers’ median of 13.57%. However, in terms of net income margin TTM, XPO slightly underperformed. XPO has a net income margin TTM of 4.48%, while its peers’ median is 5.93%.

Currently, XPO’s forward non-GAAP P/E ratio is 31.39x, higher than peers’ median of 26.61x. However, given XPO’s mixed performance against peers, I argue that XPO’s P/E should be trading closer to peers’ median. Therefore, I will be setting my 2025 target P/E for XPO at peers’ median.

For 2024, the market revenue estimate for XPO is approximately $8.19 billion, while EPS is $3.60. For 2025, the market revenue estimate is $8.79 billion, while EPS is $4.73. When analysing XPO’s 2Q24 earnings results, it did provide outlook. For 2024, XPO forecasts operating ratio improvement to be at the higher end of the 1.5% to 2.5% range due to its strong year-to-date performance. For 2025, XPO anticipates its EPS and operation ratio to continue improving. However, XPO does note that the freight market is still soft but stable. Taken together, the guidance and my forward-looking analysis as discussed support the market’s estimates. Therefore, by applying my 2025 target P/E for XPO to its 2025 EPS, my 2025 target price is $125.87.

Risk And Conclusion

For context, XPO’s business performance is highly dependent on factors such as the global trade growth rate, purchasing levels, and goods production levels. The freight industry in 2024 remains in a recessionary state, largely due to underlying supply and demand patterns.

Looking ahead, XPO provided a cautious outlook, anticipating no significant improvement in demand in the near future. For 3Q24, XPO expects the soft market conditions with flat tonnage and shipment trends to continue. On a brighter note, XPO stated that although the freight industry is currently soft, it is stable. However, if the freight industry outlook was to worsen, it could negatively impact XPO’s future financial performance.

For the quarter, XPO’s revenue grew year-over-year, driven by growth in both of its reportable segments. In addition, its adjusted EBITDA margins and adjusted net income margin also expanded. This resulted in growth in its adjusted diluted EPS. As a result of XPO’s focus and commitment to improving service quality, it resulted in an increase in yield and a decrease in damage claim percentage. Its yield reached an all-time high, while damage claims were at a record low. Overall, XPO performed well for the quarter.

link